What Is Title Insurance? A 2025 Kelowna Home Buyer's Guide

AJ Hazzi, REALTOR®

After becoming a Realtor® in 2002, AJ Hazzi noticed a gap in the real estate market...

After becoming a Realtor® in 2002, AJ Hazzi noticed a gap in the real estate market...

When you buy a home in Kelowna, you’re not just buying the four walls and a roof; you’re buying the legal rights to the property, known as the 'title'. This is where title insurance comes in. Think of it as a shield that protects your ownership from unexpected, often invisible problems rooted in the property's past.

It's a one-time fee that can save you from a world of headache, safeguarding you from hidden issues like old debts, surprise liens from unpaid contractors, or even fraudulent signatures from a previous sale.

A Kelowna Home Buyer's Guide to Title Insurance

Buying a home here in the Okanagan is one of the biggest financial steps you’ll ever take. Between viewing homes in West Kelowna, securing a mortgage, and planning your move, the closing process can feel like a whirlwind of paperwork and unfamiliar legal terms.

One term that pops up right in the middle of all this is "title insurance," and it's something our team at Vantage West Realty believes every buyer needs to get a handle on.

So, what is title insurance, really? Imagine your new home has a long history, with different owners, mortgages, and contracts stretching back decades. A lawyer’s title search does an excellent job of reviewing this known history to spot potential red flags.

But some issues simply can’t be found in public records. That’s where title insurance steps in. It protects you from the unknown—the hidden risks that could pop up and threaten your ownership years down the road.

To give you a clearer picture, here’s a quick breakdown of what these concepts mean for you as a buyer.

Title Insurance at a Glance

Concept What It Means for You

Property Title | This is your legal proof of ownership. It's the document that says you, and only you, have the right to your home. |

Title Search | Your lawyer or notary digs through historical records to ensure the seller can legally transfer the title to you, free of known issues. |

Title Insurance | This policy protects you from problems the title search couldn't find—like forgery, fraud, or unknown liens from the past. |

One-Time Premium | Unlike home insurance, you pay for title insurance just once at closing, and its protection lasts as long as you own the home. |

This table covers the basics, but the real value comes from understanding how it acts as a permanent safety net for your biggest investment.

Why It's a Safety Net for Your Investment

Think of it this way: your standard home insurance policy covers future events like a fire or a flood. Title insurance does the opposite—it looks backward, protecting you from past events that could derail your future.

For a one-time premium paid at closing, title insurance provides peace of mind for as long as you or your heirs own the property. It ensures that the beautiful Penticton home you just bought is legally and entirely yours.

Here’s a snapshot of what that protection typically covers:

Unknown Title Defects: This could be something as simple as a previous deed that was improperly recorded.

Existing Liens: A previous owner might have unpaid debts from contractors or unpaid property taxes that could suddenly be held against your property.

Fraud and Forgery: It protects you from bombshells like a forged signature on a past document that could call your entire ownership into question.

Encroachment Issues: This covers situations like a neighbour's fence that was built on your property years before you ever saw the place.

Getting comfortable with these real estate terms can feel like a lot, but they're crucial for a smooth and successful purchase. To help you get up to speed, you can explore our detailed Canadian real estate glossary for more clear, straightforward explanations.

How Title Insurance Protects Your Okanagan Investment

Okay, so what problems can title insurance actually solve? It's one thing to hear the phrase "protecting your investment," but it's another to see how it works in the real world, right here in the Okanagan.

Let's paint a picture. You’ve just moved into your dream home in West Kelowna. A few months go by, and a letter arrives from a contractor you've never heard of. It turns out they slapped a lien on the property years ago for an unpaid bill from the previous owner, and now they're looking at you to pay up.

Without title insurance, that headache is now yours. It could cost you thousands. But with a policy in your back pocket, the insurance company steps in to handle the legal mess and cover the cost.

Shielding You from Past Problems

At its core, title insurance is designed to protect you from a whole host of historical issues, often called 'title defects'. These are gremlins hiding in the property's past that are completely invisible during the home-buying process but can jump out later and threaten your ownership. Your policy is your financial shield against someone else's past mistakes.

Here are a few of the most common issues it covers:

Undiscovered Liens: This protects you from claims by contractors (a mechanic’s lien) or unpaid property or income taxes from a former owner.

Survey and Boundary Issues: It can cover you if a survey error means your neighbour’s fence is actually on your land, or if your new shed was unknowingly built over the property line.

Title Fraud or Forgery: This is a big one. It protects you if a previous deed was signed fraudulently, which could throw your ownership rights into question.

Errors in Public Records: You'd be surprised how often simple clerical mistakes at the land title office can cause massive headaches down the road.

Conflicting Wills: An unknown heir from a previous owner could suddenly pop up with a legitimate claim to the property.

Think of it like this: your property has a story that stretches back long before you came along. Title insurance ensures that a surprise chapter from the past doesn’t rewrite your future in your new home.

A Real-World Kelowna Example

Let's imagine you buy a beautiful lakeside property in Vernon. Everything seems perfect. But a year later, someone comes forward claiming they are the rightful heir from a sale that happened 20 years ago. They file a legal challenge against your title.

This is a complete nightmare for any homeowner. The legal battle to prove your ownership could drag on for years, piling up a fortune in legal fees. But if you have an owner’s title insurance policy, the insurer takes on the fight for you. They will cover your legal defence costs and, if the claim turns out to be valid, compensate you for your financial loss.

This kind of protection is vital, especially when you're making such a huge financial commitment. Understanding these risks is a key part of making smart moves, which is exactly why we put together a guide on finding the best place to invest in real estate in BC.

Understanding an Owner's Policy vs. a Lender's Policy

It’s really important to know that there are two totally different kinds of title insurance, and only one of them actually protects you. When you get a mortgage to buy a home in the Kelowna real estate market, your lender will almost always require you to buy a Lender’s Policy.

This policy protects their financial stake in your property. It’s insurance for the bank's loan, not for your investment. It simply ensures that if some old title issue pops up, the lender will get their money back.

But here's the catch: the Lender's Policy doesn't cover your down payment or the hard-earned equity you build over time. It’s all about protecting the lender’s interest, which is just the outstanding balance of your mortgage.

The Lender's Policy: Your Bank's Protection

Think of a Lender's Policy as a safety net exclusively for the financial institution that gave you the mortgage. It’s a mandatory part of most lending agreements because it’s how the bank minimizes its risk.

The coverage amount of this policy actually shrinks as you pay down your mortgage. Once you make that final payment and the loan is paid off, the Lender’s Policy just expires. It’s done its job for the bank.

A lender’s policy shields the lender’s investment in your property. Your personal investment—the down payment, equity, and future appreciation—remains unprotected without your own policy.

This is a critical distinction, and it's why understanding the second type of policy is so important for any home buyer in the Okanagan.

The Owner's Policy: Your Personal Shield

This is the one that protects you, the homeowner. An Owner's Policy is usually optional, but our team at Vantage West strongly recommends it for complete peace of mind. It’s a one-time purchase that safeguards your personal investment for as long as you or your heirs own the home.

Here's what an Owner's Policy covers that a Lender's Policy completely ignores:

Your Down Payment: It protects the initial cash you poured into the home.

Your Full Purchase Price: The policy covers the total value of your home at the time you bought it.

Future Legal Defence Costs: If someone makes a claim against your title, the insurer covers the expensive legal fees to defend your ownership.

Lasting Coverage: It stays in effect for your entire period of ownership, even long after the mortgage is paid off.

Let's use a real-world example. Say you buy a home in Penticton for $700,000 with a $140,000 down payment. The Lender’s Policy only covers the bank’s $560,000 loan. An Owner’s Policy, on the other hand, protects your $140,000 stake and the home's full value.

Without it, your personal investment is completely exposed to past title defects. Having both gives you a comprehensive shield, securing every dollar you've invested in your property.

Breaking Down the Cost of Title Insurance in BC

Alright, let's talk numbers. When clients are looking at homes in Kelowna, one of the first questions that comes up is, "What's this title insurance going to cost me?" The good news is, it’s a lot more straightforward than people think.

Unlike your property taxes or home insurance, which are recurring bills, title insurance is a one-time premium you pay at closing. That’s it. A single payment protects you for as long as you and your heirs own the property.

How the Cost Is Calculated

The cost of your policy is tied directly to the purchase price of your home. It’s pretty simple: a more expensive property means a slightly higher premium. That’s because the insurer is taking on more risk to protect a more valuable asset.

For most homes here in the Okanagan—whether it's a downtown Kelowna condo or a family home in West Kelowna—you can generally budget for a premium anywhere from $250 to over $1,000. While it varies, a common range is a fraction of the home's purchase price.

Let's put that into perspective with a real-world example:

For a $750,000 home in the Okanagan, you could expect the one-time owner's policy premium to be somewhere in the $400 to $700 range. This single payment safeguards your entire investment against any hidden title issues from the past.

Factors That Influence the Final Price

A few key things can nudge the final number on your invoice. Knowing what they are helps you see exactly what you're paying for.

Home Value: This is the big one. The policy has to cover the full purchase price of your property, so it’s the primary driver of the cost.

Property Type: The kind of property you’re buying (like a detached house versus a strata unit) can sometimes influence the final premium.

Bundling Discount: Here’s a great way to save a few bucks. When you buy your Owner’s Policy and the required Lender’s Policy at the same time, most insurers offer a pretty hefty “simultaneous issue discount” on the lender’s portion.

When you look at it, this upfront cost is a tiny price to pay for the long-term security of what's likely your biggest financial asset. It's all about making sure your ownership is rock-solid, so you can build your future here in the Okanagan with total confidence.

The Title Search and Insurance Process Step by Step

So, how does all of this actually play out when you’re in the middle of buying a home? It can feel like a lot is happening behind the scenes with your lawyer, but the process is actually quite logical. It's all designed to make sure the keys you get on closing day come with clear, undisputed ownership of your new property.

It all kicks off with the title search. Once your offer on a Kelowna home is accepted, your lawyer or notary springs into action. Think of them as property detectives, digging through years of public records tied to your soon-to-be address.

Conducting the Title Search

This isn't just a quick skim of the paperwork. Your legal team meticulously combs through a mountain of documents to piece together a complete history of the property. They’re on the hunt for any red flags that could cause you serious headaches down the road.

This deep dive includes checking:

Deeds and Transfers: To confirm a clear and unbroken chain of ownership.

Mortgages: To ensure all previous loans against the property have been properly discharged.

Tax Records: To verify there are no surprise property tax bills waiting for you.

Court Judgments: To uncover any liens or legal claims filed against the property.

The ultimate goal is to find what’s called a 'clear title,' which means there are no known issues that could threaten your ownership. The information uncovered here is very different from what a seller provides; for a deeper look into seller disclosures, check out our guide on the Property Disclosure Statement.

From Search to Insurance Policy

What if the search does turn up a problem? Don't panic. For minor issues, like an old mortgage that was paid off but never officially removed from the records, your legal team will work to resolve it before closing day. "Curing" the title is a standard part of their job.

This is also the point where the title insurance company steps in. Using the results of the title search, they assess the property's risk level. If the title is clear—or once minor issues are cleaned up—they’ll issue your policy.

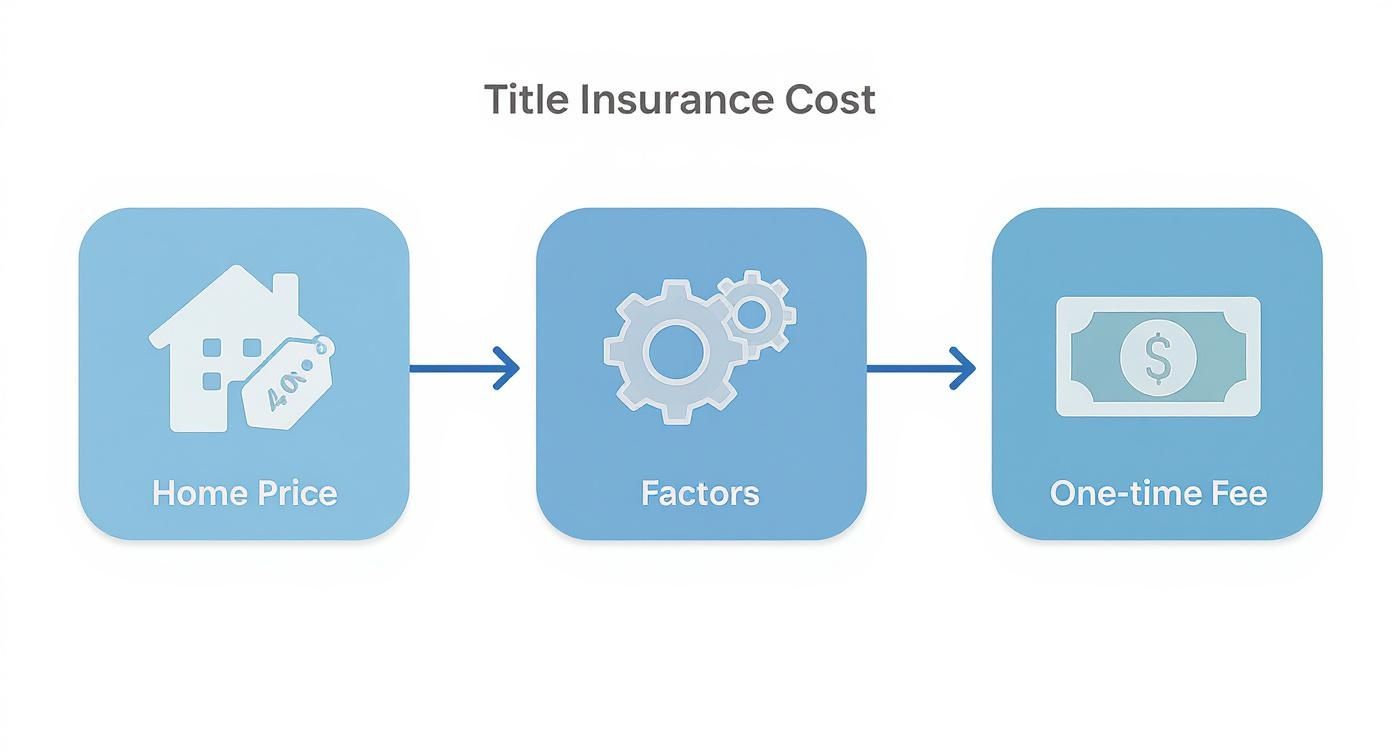

This infographic breaks down how these key elements come together.

As you can see, it’s a pretty straightforward progression from the property's value to the final protective fee.

Now, what if a serious risk is found that can't be resolved? The title insurance company might still issue a policy but will list that specific risk as an "exception," meaning it won't be covered. More often, though, they will insure you against any claims that could pop up from undiscovered problems—the kind that even the most thorough search couldn't possibly find.

This step-by-step process ensures you’re protected from both the known and the unknown, giving you the confidence to move forward with your purchase of a home in the Okanagan.

So, what happens if you actually need to use your title insurance? While you hopefully never will, knowing the process is incredibly reassuring. This is the moment your one-time investment proves its true worth, protecting your slice of the Okanagan.

An issue can pop up months or even years after you’ve settled in. It might be a previous owner's long-lost heir suddenly making a legal claim on your property, or you could uncover an old municipal work order demanding expensive upgrades you knew nothing about.

Taking the First Step

If a potential title issue comes to light, your very first move should be to call your title insurer. Right away. Don't try to solve it yourself or hire a lawyer on your own—your policy requires you to notify the company promptly so they can jump in from the very beginning.

They'll connect you with a claims professional who will guide you through what they need.

Typically, you'll need to have these on hand:

A copy of your title insurance policy.

Any letters or legal documents you've received about the claim.

A detailed written explanation of what's happening, as you understand it.

Here's the most powerful part of your policy: the title insurance company takes on the entire legal and financial burden. They are on the hook for your legal fees and any financial losses, right up to your policy's full value.

How the Insurer Responds

Once you've filed the claim, the insurer’s legal team gets to work investigating. They handle all the back-and-forth with the other parties, bring in lawyers if needed, and focus on shutting down the problem. This whole process is designed to defend your ownership rights without you having to spend a single dollar on your legal defence.

This is the ultimate peace of mind. Your policy isn't just a piece of paper; it's a powerful shield protecting your financial future, letting you enjoy your Kelowna home without worrying about ghosts from its past.

Your Top Title Insurance Questions Answered

When you're buying a home in Kelowna, terms like "title insurance" can sound complicated. We get it. Here are some of the most common questions we hear from our clients at Vantage West Realty, broken down into clear, straightforward answers to help you buy with total confidence.

Is Title Insurance Mandatory in British Columbia?

No, an Owner's Title Insurance policy isn't legally required for a home buyer in BC. That said, your bank will almost certainly require you to purchase a Lender's Policy to protect their mortgage investment.

Our team at Vantage West strongly recommends getting an Owner's Policy for yourself. It’s a relatively small one-time cost that protects your biggest investment—your down payment and all the equity you build over the years.

How Long Does Title Insurance Coverage Last?

Forever. Well, for as long as you or your heirs own the property, anyway. You pay a single premium when you close the deal, and that's it. No renewals, no annual fees.

Just remember, the policy doesn't transfer to the next owner when you eventually sell. They'll need to get their own policy to be protected.

Think of it this way: the title search shows the property’s documented history, while title insurance protects you from the financial fallout of problems that even the most thorough search could never reveal.

Isn't My Lawyer's Title Search Enough Protection?

A lawyer’s title search is an absolutely essential step, but it only shows what’s available in the public record. It can’t see the things that are hidden.

What it won't catch are the nasty surprises like a forged signature on a past deed, an unknown heir who suddenly makes a claim, or a simple clerical error at the land registry office from decades ago. These are exactly the kinds of issues that can crawl out of the woodwork years later, landing you in a world of legal and financial stress.

The title search is a critical look at the property's known past. The insurance is your shield against the unknown. For anyone buying in the Okanagan real estate market, it’s a vital layer of security.

Navigating the details of buying or selling in Kelowna doesn’t have to be overwhelming. At Vantage West Realty, we guide you through every step with clear advice and expert support. If you're ready to make your next move with confidence, reach out to our team today.

Sell Your House With Vantage West Realty

Sell your home on your own time with the Vantage West Guaranteed Home Sale Program.

if your home doesn’t sell in a mutually agreed upon timeframe, we’ll provide you with a guaranteed written offer.